Prepaid Card Strategy: Structural And Regulatory Foundations

"I already have a credit card, why would I need a prepaid card?"

This is a question that seems perfectly reasonable at first glance in the financial sector, yet it conceals a fundamental assumption. The idea that everyone has a credit card or a debit card, and that these two products cover every need, does not fully reflect reality.

According to the World Bank's 2021 Global Findex report, roughly 24% of the global adult population remains unbanked. These individuals may have income and employment, but without a formal credit history, a bank account, or documented proof of employment, their credit card applications are simply not considered. Age, citizenship, or other factors can also prevent them from obtaining a debit card, since that requires a bank account. So if these two payment methods already exist, why do major banks keep issuing prepaid cards? And why do newly established payment institutions build their entire portfolio around this single product as their primary offering?

In this article, we'll look at what a prepaid card actually is, the scenarios where credit and debit cards fall short, why even major banks are investing in this product, and how the regulatory framework has shaped this choice.

Image 1: Comparison of Three Card Types (Credit, Debit, Prepaid)

Three Cards, Three Different Logics

Card-based payment systems rest on three core instruments, each built on a different financial logic.

- Credit card works on a short-term credit line extended by a bank. The user spends first and pays later. Credit limits, delinquency management, and collections are inseparable parts of this product, and a credit assessment is mandatory.

- Debit card tied to the balance in the user's existing bank account. Funds are deducted in real time, so there's no credit risk. However, it requires a bank account, and opening one requires identification, proof of address, and in some countries a minimum balance.

- Prepaid card tied to neither a credit line nor a bank account. Users spend only what they've loaded onto the card. By design, it doesn't allow spending beyond the loaded balance, and it requires no bank account or credit history.

The difference between these three products isn't just technical — it's also about who they can actually reach.

Why Prepaid When Debit Already Exists?

This question raises a subtler objection than the credit card one. Debit cards are also balance-based, carry no credit risk, and work fine for everyday spending. So where's the difference?

1. A Bank Account Is a Precondition

A debit card is, by definition, tied to a bank account — and opening one, while seemingly simple, is often a process full of real obstacles: identification documents, proof of residence, minimum balance requirements in some cases, and tax ID requirements in others. Migrants, tourists, seasonal workers, parts of the elderly population, and minors may not be able to clear these hurdles. For this segment, a prepaid card is the only electronic payment instrument accessible without a bank account.

2. Account Security and Risk Mitigation

A debit card gives direct access to the user's entire account balance. If the card details are stolen or an unauthorized transaction occurs, the whole account balance is at risk, and the refund process can take time. With a prepaid card, the maximum possible loss is limited to the balance loaded onto the card. This structure provides strong risk mitigation, particularly for purchases on platforms of uncertain reliability or for recurring subscription payments — the user protects their main account while transacting with a balance set aside for a specific purpose.

3. Spending Control and Category Management

Since a debit card grants access to the full account balance, spending discipline is left entirely to the user. A prepaid card, by contrast, can have structural limits built in — a card can be created with a fixed amount, restricted to a specific category, or limited to a specific time window. This offers a flexibility and security that debit cards can't match, particularly useful for corporate expense management, parental controls, and budgets set aside for a specific project or trip.

4. Anonymous or Partial Identity Verification

Regulatory frameworks can allow simplified KYC (Know Your Customer) procedures for low-limit prepaid products. Access to the electronic payment system at a limited level, without full identity verification, is something a debit card can never offer.

Image 2: Debit Card vs. Prepaid Card

Why Are Major Banks Developing Prepaid Cards?

Another key question: why would established financial institutions, which already have both credit and debit card portfolios, bother developing a prepaid product as well? According to Capgemini's World Payments Report 2023, a significant share of global payment institutions position prepaid products as their primary customer acquisition tool. Global banks like JPMorgan Chase, Bank of America, BBVA, and ING have been unable to ignore this dynamic and have built out their own prepaid card portfolios. Looking at these banks' statements and published industry reports, a common motivation emerges: reaching customer segments that existing products can't serve.

Younger Populations and Digital Natives:

Individuals under 18 legally cannot use a credit card, and a debit card must be tied to a parent's account. A prepaid card gives this segment an independent payment experience. Banks see this product as a strategic tool for building early relationships with future customers — the youth-focused prepaid product launches from major banks confirm this strategy. Platforms like Greenlight (US-based, working in partnership with major banks), GoHenry (UK), and Kard (France) have positioned parent-controlled prepaid cards as the primary financial product for the youth segment and have received investment from major banks.

Expense Management and the Corporate Segment:

Prepaid solutions aimed at corporate clients are another strategic area for major banks. Visa Commercial Solutions and Mastercard Corporate Prepaid programs illustrate how major banks worldwide have adopted prepaid infrastructure for corporate expense management. Travel expenses, supplier payments, and project-based budget management are the primary use cases here. For example, foreign exchange conversion fees on credit and debit cards create significant additional costs during international travel. Multi-currency prepaid cards preloaded in a specific currency both limit exchange rate risk and make spending budgets more predictable. This exact scenario has been one of the core drivers behind the global scale reached by Wise and Revolut.

Brand Expansion and Adjacent Ecosystems:

Banks view the prepaid card not merely as a payment instrument but as an entry point into a broader ecosystem. Co-branded prepaid cards issued jointly with a specific retail chain or digital platform give both the bank and its partner cross-access to each other's customer base. In this model, the prepaid card becomes a brand-expansion tool for the bank.

Image 3: Major Banks' Prepaid Card Strategy

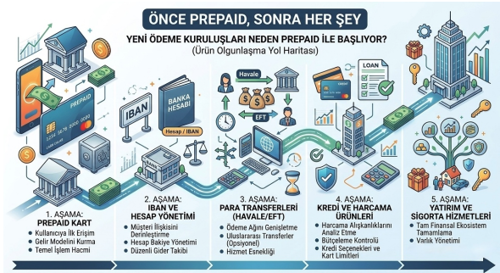

Why Do New Payment Institutions Start With Prepaid?

Licensing and Regulatory Structure:

In Turkey, issuing a credit card requires a banking license under the Banking Law. Payment institutions and e-money institutions operating under Law No. 6493, however, can issue prepaid cards under the supervision of the Ministry of Treasury and Finance and the Banking Regulation and Supervision Agency (BRSA).

Image 4: Comparison Criteria

No Credit Risk Exposure:

Both credit and debit cards require the issuing institution to take on certain operational risks. For credit cards, this translates directly into credit risk; for debit cards, it involves account management, liquidity, and fraud risk. With a prepaid card, the customer can only spend what they've loaded — credit risk doesn't scale proportionally as the customer base and transaction volume grow. This is a fundamental advantage for growth-focused payment institutions and translates into a predictable risk profile for investors.

Speed, Testability, and Data:

Prepaid card infrastructure can be built without a credit assessment engine, a limit management system, or a collections mechanism, which allows the product to reach the market much faster. A payment institution can follow a path like this:

- Launch a basic prepaid card.

- Observe user behavior, spending patterns, and preferred categories.

- Use this data to develop more layered products.

- Once sufficient customer base and data have been accumulated, move into more complex financial products.

In this process, the prepaid card functions as both a product and a data collection tool. Spending categories, transaction times, geographic distribution, and reload behavior form a valuable foundation for personalized product development and risk modeling down the line. This pattern is clearly visible in European payment institutions like Revolut, Wise, and N26, all of which began this journey with a prepaid-centered product and gradually built out deeper financial product portfolios to reach global scale.

Image 5: Product Maturity Roadmap

Regulatory Framework: The Legal Basis of Prepaid Cards

The core regulatory framework for issuing prepaid cards in Turkey is shaped by the following documents:

- Law No. 6493: The general framework for payment services and e-money issuance

- Regulation on Payment Services and Electronic Money Issuance and on Payment Institutions and Electronic Money Institutions: Operating conditions and product requirements

- MASAK (Financial Crimes Investigation Board) regulations: Customer identity verification (KYC) and anti-money-laundering obligations

KYC requirements can be applied to prepaid products in tiers: low-limit products can be offered with simplified identity verification, while limit increases require more extensive verification steps. This tiered structure is deliberately designed to enable broad access while maintaining regulatory compliance at the same time. In Europe, the PSD2 and EMD2 frameworks have made prepaid and e-money products the backbone infrastructure of the fintech ecosystem — these regulations have eased market entry, increased competition, and paved the way for the rapid spread of innovative payment solutions.

Conclusion: Not an Alternative, But a Complement — and Sometimes the Primary Choice

Credit and debit cards are well-established, robust products within the financial system. But individuals without a bank account, those without a credit history, those who want to structurally limit their own spending, organizations looking for corporate budget management, and situations requiring a specific risk safeguard — these are all areas that credit and debit cards simply can't reach. Major banks, recognizing this, have directed part of their efforts toward this space and continue to do so. New payment institutions, meanwhile, have adopted the prepaid card as their primary strategic tool to cover this space with the lightest possible capital burden, the fastest speed, and the most scalable structure. A prepaid card isn't an alternative to credit or debit cards — it's a complement that illuminates the blind spot these products can't see, and for certain segments, it's the primary financial tool.

The evolution of payment systems isn't heading toward a single product that meets every need — it's moving toward an ecosystem of complementary tools, each purpose-built for a specific need. In my own view, the prepaid card will remain one of the oldest and, at the same time, one of the most dynamic links in this ecosystem.

One of BOACard's standout strengths is its complete support for all three core card types — debit, credit, and prepaid — on a single platform. As financial needs continue to diversify, being able to manage all three card types on the same infrastructure gives banks a serious competitive edge, both in operational efficiency and in the breadth of products they can offer their customers. With BOACard, a bank can roll out debit cards for payroll and current-account holders, credit cards for customers with shopping and installment needs, and prepaid card solutions for those seeking budget management or corporate expense control — all from a single system, with a single integration. For more information, you can visit the BOACard website.

References

- All images in this article were generated using artificial intelligence with Google Gemini.

- World Bank — Global Findex Database 2021

- BIS — Payment Aspects of Financial Inclusion in the Fintech Era (2020)

- Capgemini — World Payments Report 2023

- GSMA — State of the Industry Report on Mobile Money 2023

- McKinsey & Company — McKinsey Global Payments Map 2023

- Law No. 6493 on Payment and Securities Settlement Systems, Payment Services, and Electronic Money Institutions

- Ministry of Treasury and Finance — Regulation on Payment Institutions and Electronic Money Institutions

- Directive 2015/2366/EU — Payment Services Directive (PSD2)

- Directive 2009/110/EC — Electronic Money Directive (EMD2)

- Visa — Visa Commercial Solutions: Corporate Prepaid Program Overview

- Mastercard — Mastercard Corporate Prepaid: Expense Management Solutions

- Spendesk, Pleo, Soldo — Corporate expense management platform documentation

- Greenlight Financial Technology — Product Overview and Partnership Framework

- GoHenry — Annual Impact Report 2022